Current page

Arcus

Arcus enables two trading mechanisms side by side. Perpetual futures trade on a central limit order book. Stock Tokens trade spot through a request for quote (RFQ). That isn't an accident of engineering history, it's a deliberate answer to a question most venues never ask: what does this market actually need?

Order books and RFQ aren't rivals where one is modern and the other legacy. They're tools with different properties, and the honest way to build an exchange is to match the tool to the market.

Where the Order Book Earns its Place

A central limit order book (or a CLOB) is a great price discovery machine built for markets with continuous two sided flow. Standing bids and offers compete in the open, competition compresses spreads, and everyone sees the same depth.

Arcus perps live in exactly that environment. Perps are instruments for trading price, so the book itself is where price gets discovered. They run 24/7 by construction, settle in USDG, and leverage concentrates volume into deep, active markets. Makers can rest orders with confidence because the flow that keeps those orders fresh hardly stops.

Stock Tokens are a Different Market

The real question is whether Stock Tokens share those properties. They don't, in three specific ways:

Fair value lives somewhere else: A perp's price is discovered on the book. A Stock Token provides economic exposure to an underlying security whose price is set on traditional markets. The venue isn't discovering the price so much as delivering it, plus a spread that reflects the cost of hedging.

The hours don't align: Stock Tokens trade around the clock while the underlying keeps exchange hours. A resting order placed Friday afternoon can be stale by Sunday night, mispriced against every headline in between. Makers know this, so they either quote defensively wide or don't rest orders at all.

Depth is still building: Stock Tokens are a novel asset class, and the continuous flow that keeps a book tight doesn't yet exist in the long tail.

Force this market onto a CLOB and you can get thin books, wide spreads, and stale quotes on names where the underlying just moved. Rely on passive AMM pools alone and prices follow a formula rather than information, correcting only when arbitrage extracts the difference from liquidity providers. Neither failure is hypothetical in thin markets.

RFQ: Liquidity on Demand

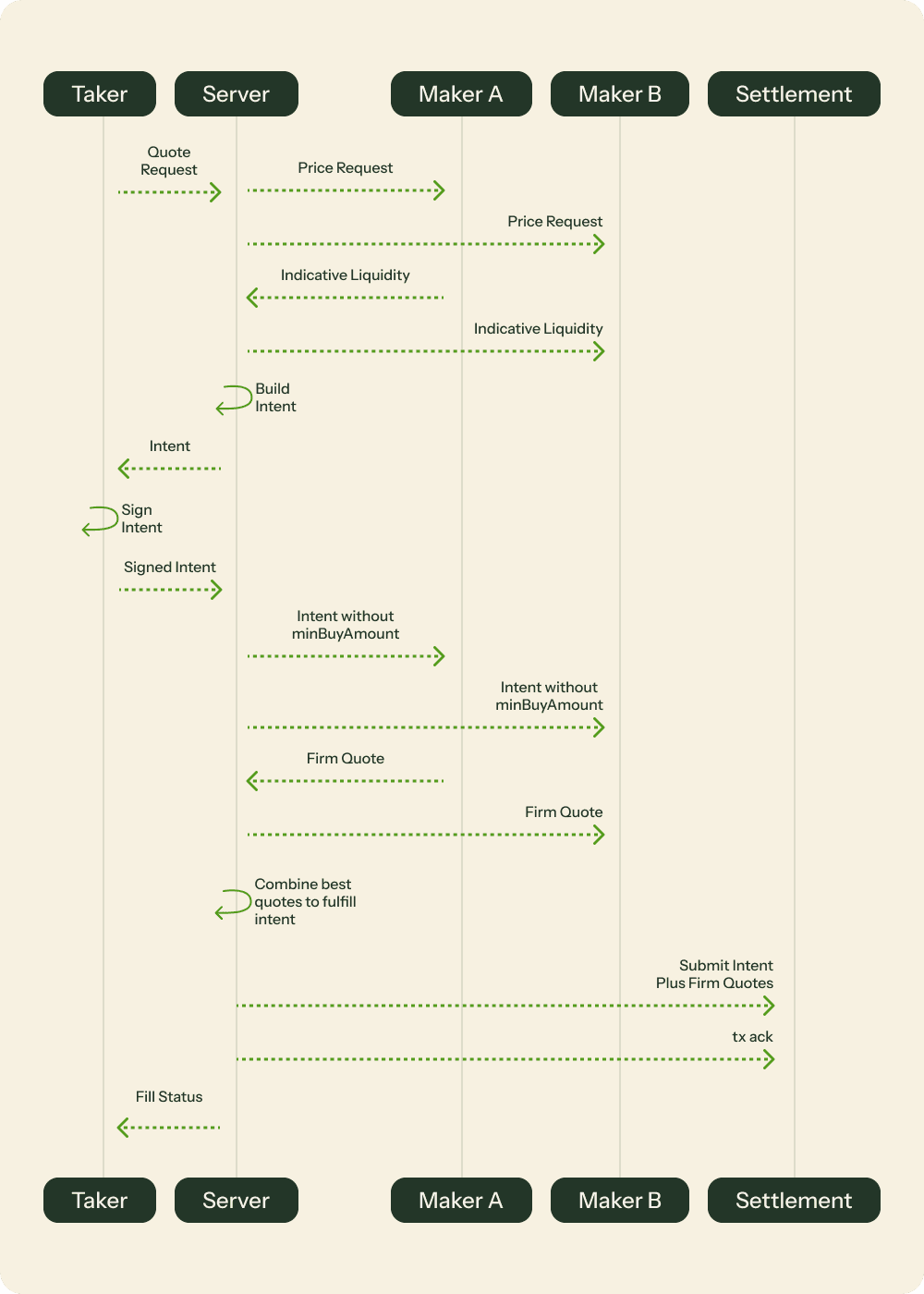

RFQ inverts the resting liquidity model. Rather than makers warehousing quotes and waiting, the trader asks for a price, and professional makers compete to fill that exact trade, at that size, in that moment, with current information about the underlying.

On Arcus, the flow works like this:

Quote: You request a trade by sending your trade parameters: what you're selling, what you're buying, the size. The server polls market makers for indicative pricing and builds an intent: the trade you're committing to, including the minimum amount you'll accept.

Sign: You sign the intent from your own wallet. This is the key trust boundary in the whole system. Your signature authorizes this trade and only this trade, bounded by your minimum. Execution can settle better than the estimate, but never below your floor.

Firm quotes: The server forwards the intent to makers, deliberately without disclosing your minimum. Makers can't price against your limit, so they price the trade on its merits and return binding, signed quotes.

Settlement: The server assembles the most optimal combination of firm quotes to cover your full size, bundles them with your signed intent, and submits a transaction to the settlement contract. Every leg settles atomically: all fill, or none do, and you see the result.

Three Design Choices Worth Reinforcing

Your limit stays hidden: In most quoting systems, revealing your minimum price is an invitation to be filled exactly at it. Trading on Arcus keeps your minimum limit on the server side, allowing makers to only see the trade (asset, size and direction), but not your tolerance. They therefore compete blindly against each other rather than against your limit. The server enforces your floor when it assembles the fill plan, and any plan that doesn't clear it never gets submitted.

Quotes are firm and combinable: A maker's quote is a signed, binding commitment. The server can take all or part of each one, stitching multiple makers together to cover a single order at the most optimal aggregate price. From your side, there's one trade and one outcome. The routing is the server's problem.

Settlement is atomic and non-custodial: The signed intent and the selected quotes execute in one transaction. If any leg fails: a quote expired mid-flight or a balance moved, the entire transaction reverts. Nothing transfers, funds stay in your wallet, and the app tells you the trade didn't complete.

What this Feels Like in Practice

In practice, the mechanics above collapses into a simple experience: you request a price, see an all-in quote, confirm the price, and receive the Stock Tokens. Trades are currently gasless, and there's no partial-fill limbo: either the trade completes at or above your floor, or nothing happens.

It also explains a behavior that surprises anyone expecting an order book. Quotes expire within seconds, because a firm price against a live underlying can't sit around. Outside US market hours, spreads widen and a thin name may briefly return no quote at all. This is the system being honest about what the makers can hedge, whereas a stale order book can hand you a dishonest fill.

Makers Benefit Too

RFQ removes the tax of resting in a market that punishes resting: no orders picked off on an overnight gap, no pool capital bleeding to arbitrage. Capital commits only when a quote is selected, which lowers the cost of quoting, and, over time, that's what tightens spreads.

The Principle

None of this amounts to "RFQ good, order books bad." The point is that market structure should follow market properties. Where price is discovered on the venue and flow is continuous, i.e. perpetuals, a CLOB is unbeatable, and Arcus enables one. Where fair value is set elsewhere, hours misalign, and liquidity needs to be summoned rather than parked, i.e. Stock Tokens, RFQ fits the shape of the problem.

Most venues pick one mechanism and force every market through it. Arcus built both, and put each market on the structure it deserves.

—-

Arcus is a blockchain-based smart contract protocol that permits self-custodial peer-to-peer trading of Stock Tokens, cryptoassets and perpetual futures. Arcus is not a regulated financial services provider, and it is not available in the U.S., Canada, United Kingdom and other restricted jurisdictions.

Stock Tokens are tokenized securities that provide economic exposure to a relevant underlying equity instrument or ETP through a contractual claim against the Issuer for a cash Redemption. Stock Tokens involve risks not present, or not present to the same extent, in traditional stock ownership, including private-key loss or compromise, limited redemption access, liquidity constraints, price or tracking divergences from the underlying, and uncertain or evolving regulatory treatment.

Trading Stock Tokens, cryptoassets or perpetual futures is risky and involves risks of loss, particularly when using leverage. Do your own research.

This content is provided as a general tool for users to learn about or interact with Arcus on their initiative, with no endorsement or recommendation of any trading activities. Users or potential users of this content should not regard it as involving any form of recommendation, invitation or inducement to deal in Stock Tokens, cryptoassets or perpetual futures. Nothing herein should be used as legal, financial, tax, or any other form of advice.

In no event will Pocket Protector Labs Inc. or its affiliates be liable for any loss or damage arising from or in connection with the use of Arcus or this content. By continuing to access this content, you agree to the Interface Terms of Use, Protocol Terms and Privacy Policy.

Market analysis is facilitated with charts by independent third party service provider(s).

What is Arcus?

Arcus is a decentralized exchange built in partnership with Robinhood on Robinhood Chain. Users from eligible jurisdictions get one self-custodied account to trade Stock Tokens (spot, zero fees, 24/7), and cross-margined perpetual futures across equities, crypto, commodities, and indices - 24/7, with up to 50x leverage.

When is Arcus Launching?

Arcus is live in Beta. Spot Beta is open now to all eligible users, no waitlist needed. Perps Beta opens July 1, 2026, starting with waitlisted users and rolling out by cohort, ahead of a full launch later in the year. Join the waitlist and we'll let you know when your cohort opens. Arcus isn't available in the United States, United Kingdom, Canada, or other restricted jurisdictions, as set out in the Terms of Use.

What's the connection to dYdX?

Arcus is the next chapter for the team that built dYdX. dYdX Chain continues to operate. Arcus introduces new asset classes - equities, indices, commodities - alongside crypto perps, on a chain purpose-built for the throughput these markets require.

How does the waitlist work?

Only perps are waitlisted; Spot Beta is open to all eligible users. To join the waitlist, visit waitlist.arcus.xyz, and connect your wallet and X account. Your position comes down to two things: your prior on-chain trading history (perps volume across venues like dYdX, Hyperliquid, and Lighter, with real-world-asset (RWA) volume as a bonus), and referrals of other validated traders. You can connect multiple wallets to aggregate your history and move up faster. The earlier you join, the earlier you trade.

Where can I learn more?

Read the Arcus blog, follow @arcus_xyz on X, and join our Telegram for live updates.